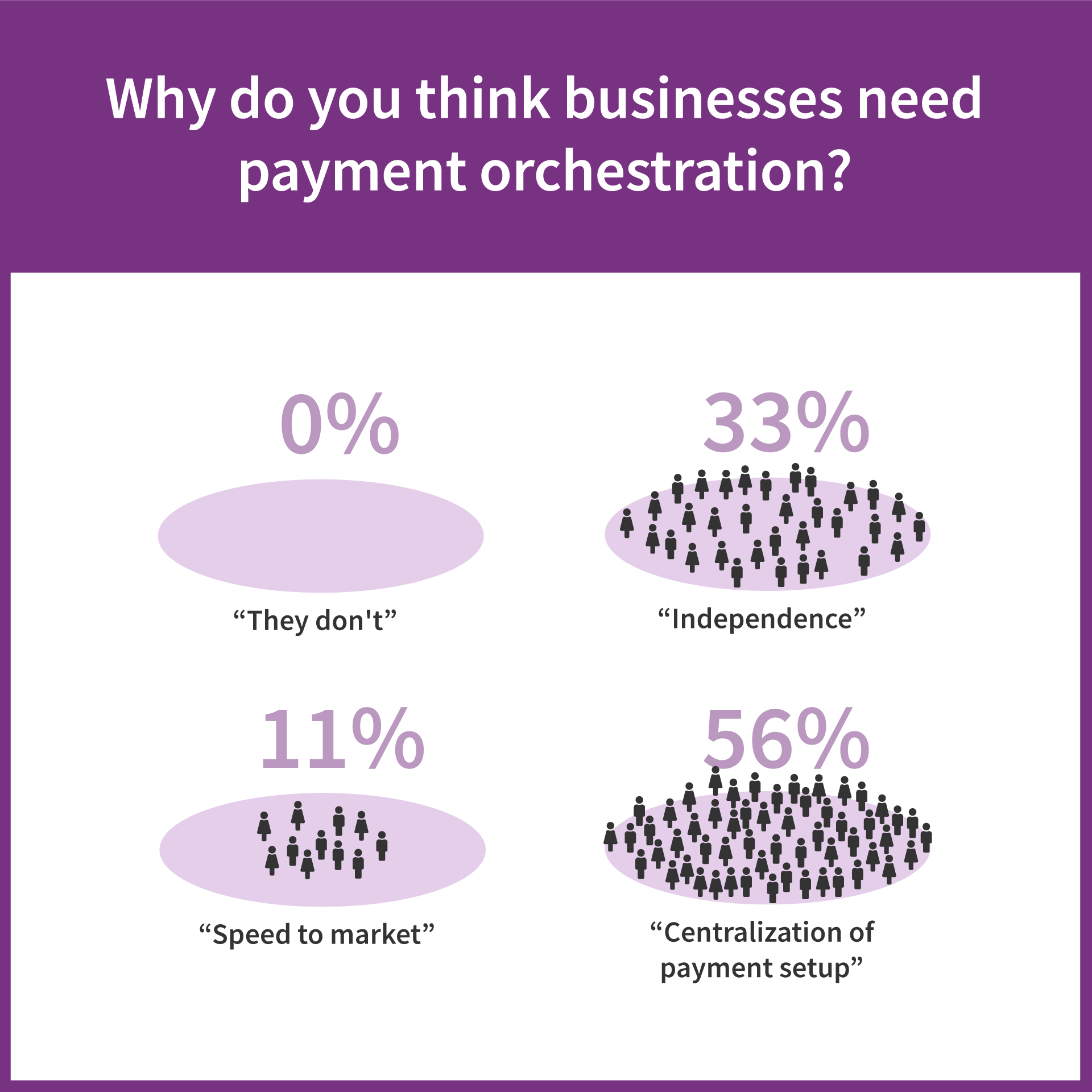

On April 22, 2021, IXOPAY and PaymentsOp held a joint webinar on how payment orchestration is redefining the merchant experience. It was an interesting and varied session that covered a lot of topics. Below is a summary of what was discussed and the key points for all those who could not attend.

Keren Aviasaf, the CEO of PaymentsOp looked at three different case studies and how each of them benefited from having a centralized solution for their payments stack.

Case Study #1: ISVs that move into Payment Facilitator Model

Payment facilitation (PayFac) has grown in popularity due to the combination of potential hyper growth and instant on-boarding. However, many software providers cannot understand or underestimate the full payment facilitation picture. Worldwide, there’s approximately $120 trillion in B2B transactions every year. The B2B tech platforms that facilitate a respectable chunk of these transactions do not make any money from them. PayFacs (like Stripe) are willing to share a portion of the payment processing revenue, and ISVs have realized that it is not only an excellent additional revenue stream but also a valuable service for customers who would otherwise have to integrate a payment solution.

Why don’t these B2B platforms become PayFacs themselves and take all the revenue?

Doing so is complicated. The underwriting process is long and grueling, and PayFacs are responsible for any fraud or chargebacks on their platform. Integrated payments are the better choice for most ISVs. Using a Payment Orchestration Platform lays the foundation for best practice underwriting and monitoring policies & processes. Some of these systems have capabilities:

KYC & KYB tools (including forms wizard)

Risk Rules engine

Velocity & limits

Dashboard & customised reports

Even though the ISVs may decide to take only financial liability and leave the compliance to their partner PayFac, there is still a reputation risk to be managed.

Each company needs to ask themselves how deeply embedded into payments they want to become

Case Study #2: Marketplaces complex operation of Pay-In & Pay-outs

Most marketplace platforms will tell you they are product oriented, although they process a high volume of transactions, they never see themselves as banks. They handle hundreds of operational procedures, but may experience a shortfall in the technological infrastructure of processing & billing.

It is imperative that they “get it right”, otherwise they are left holding the chargeback bag and do not have enough volume elsewhere in their account to cover the card association/acquirer thresholds in order to remain solvent & profitable. While they want the process to be quick/easy/painless, it needs to be thorough.

They need a balance in order to allow payouts for vendors & affiliates. It is normal that they have to support different payment models:

% of the transactions is paid to a vendor

% of group of transactions from different customers is paid to a vendor

Fixed amount on each transaction is paid

A % up to a minimum or max amount to be transferred

Different time scheduling can make things even more complex

Case Study #3: Optimize & Scale Merchants Global processing

The use of Payment Orchestration Platforms for global merchants is overwhelming:

Streamline payment operation in one place

scale, localization, short TTM

Approval Rates - pre & post processing optimization

Monitoring & Insights in a consolidated view

Some merchants used five or more payment systems in tandem to cover multiple geographic regions and payment methods, or perhaps to support a different business model. The multiple integrations were expensive to engineer and maintain. Aggregating and standardizing data from multiple payment systems was difficult, and development teams spent more time writing to different software than investing in their own product.

Many businesses are finding they can reduce expenses and minimize technical debt with an all-in-one payment solution. The right platform can lower costs while providing access to additional payment methods and local acquiring banks in cross-border markets.

Payments is not a commodity it is a proficiency

Adam Vissing, Vice President of Business Development and Sales at IXOPAY, looked at some of the questions merchants ask themselves when looking at their payment solution, how payment orchestration can be integrated and its technical capabilities.

The commerce landscape has been through a radical transformation within the last year. Because of covid, many businesses had to quickly pivot most or all of their operations online and therefore needed a much more robust process for online payments. The eCommerce landscape was then shaken by the demise of Wirecard which left many businesses scrabbling to reorganize their payment stack.

Many had to ask themselves some tough questions:

...are they fast enough?

...are they flexible enough?

...are they resilient enough?

...can they deal with the complexity?

In order to get the speed, flexibility, resilience and ability to handle complex requirements, merchants can process their transactions through a payment orchestration platform. Through just one, API merchants can connect to multiple payment service providers and third party risk and fraud solutions.

What needs to be done in order for a merchant to successfully set up payment orchestration?

Preliminary Work:

Build a catalogue of existing providers, endpoints, methods, contracts & internal processes

Identify 3rd-party data silos (e.g. PSP Tokens) & applications (e.g. for Risk Management)

Define reconciliation formats & transport mechanisms, document “stakeholder” systems

POP Vendor Selection:

Map POP vendor functionality & connectivity to requirements

Evaluate vendor dependencies (Organizational & Technical)

Commercials & SLA

Implementation:

Configuration of POP Platform

Integration of e-Com Front-ends, Line-Of-Business Apps with POP

Data Migration & Go-Live (Tokens, Transaction History, etc.)

There are many things to consider when switching to a payment orchestration platform, and of course every merchant wants to know how long it will take. On a technical level, the basic integration of a POP is roughly comparable to the integration of a PSP. However, POP Projects are a consolidation / rationalization opportunity. Migrating a complex legacy payment set-up to a POP requires a dedicated project team. There will be higher initial costs, but merchants will see a quick return on their investment once the system is up and running.

Project pitfalls to be weary of:

A POP does not absolve merchants from managing PSP relationships

POP connectivity is more than a list of PSPs

POPs are expert platforms and require skilled, knowledgeable owners

If you don’t have a “Head of Payments” on your team, better start looking for one!

What are the benefits of Payment Orchestration?

Transaction Routing - routing is applicable primarily to Credit Card and Bank Transfer (e.g. DD) Transactions

Primary goals of routing are always to

increase authorization rates

compress fees

ensure resiliency / reduce risk

Popular Strategies implemented via POPs:

Local Acquiring

Load Balancing / AB Testing

Failover / Cascading

Risk-Based Routing

There is no single “best” approach to transaction routing - each Merchant’s strategy is individualized

Risk Management - nearly every PSP offers an individual approach to Risk Management. However, global merchants seek to consolidate and improve Risk Management Practices POPs can help by:

Providing a built-in Risk Management Layer, applicable to all TRX regardless of target PSP

Screen transactions before they “hit” the Acquirers / Schemes

Managing SCA Challenge and Exemption Requests

Facilitating the integration/orchestration of specialized 3rd-Party Risk Solutions

Typical Risk Checks include Geo / IP address, Velocities, Device Identification/Fingerprinting

Reconciliation - Working with multiple PSPs means dealing with multiple settlement formats and procedures Reconciling this data with Line-of-Business applications (e.g. ERPs) is often a challenge. POPs can help by:

Fetching and processing settlement data from PSPs and Banks

Verifying settlement data (e.g. correct fees being applied to transactions)

Providing a consolidated, yet customizable reconciliation format via various transport methods

Enabling flexible scheduling of reconciliation data flows

Automation of these processes is one of the most important ROI drivers in POP projects

Sounds complicated?

It is. But with a payment orchestration platform, the hard work is done for you.

Watch the webinar in full

Sign up to our newsletter and follow us on social media

To stay up to date on payments topics

RegisterAbout PaymentsOp:

PaymentsOp is a boutique advisory firm providing guidance in the field of e-Payments, Risk & Fraud Prevention, Payment Data Security, and Compliance. Their vision is to provide professional knowledge and comprehensive accompaniment to any organization operating in e-Commerce around the world. PaymentsOp accompanies businesses through the process mapping, development, and implementation providing services that lay the foundation for sustained top line growth. PaymentsOp is the perfect partner for all companies that strive to improve their payment processes while simultaneously reducing costs. They have a great reputation for serving diverse businesses that offer digital or physical goods and services online through web sites and mobile apps.

Please find more information about PaymentsOp here: https://www.paymentsop.com/

About IXOPAY

IXOPAY is a payments orchestration platform enabling independent, flexible and global payment processing. As a highly scalable and PCI-DSS certified “fintech enabler”, IXOPAY fulfills the needs of large merchants as well as those of “white label” clients: payment service providers (PSPs), acquirers and independent sales organizations (ISOs). The modern, easily extendable architecture offers smart transaction routing & cascading, state-of-the-art risk & fraud management, fully automated reconciliation and settlements processing, comprehensive reporting as well as plugin-based integration of acquirers, payment service providers and alternative payment methods (APMs).

IXOPAY is part of the IXOLIT Group, founded in Vienna, Austria in 2001. With local entities in Austria and the USA, IXOLIT supports national and international customers across various industry verticals. The owner-led and -financed company has grown from 2 to more than 65 employees and is focused on building innovative solutions for eCommerce.

Please find more information about IXOPAY here: https://www.ixopay.com