When managing payments at scale, it's easy to focus on topline revenue and overlook the invisible costs eating your margins: processing fees, scheme costs, interchange, and service markups. Yet for CFOs and Head of Finances, understanding these fees-and how they appear across provider invoices-is essential to ensure accuracy, minimize leakage, and negotiate smarter.

In this blog post, we'll break down how fees work in the payment ecosystem, how they're billed by PSPs (Payment Service Providers), and how to manage and reconcile invoices effectively.

Introduction to Fees and Costs in Payments

Payment processing fees are the costs businesses incur to accept and process payments, whether through credit cards, digital wallets, or bank transfers. These fees are a combination of several components, each tied to different aspects of the payment lifecycle. Payment flows can become very complex and vary for payment methods and channels, making it vital for CFOs to understand the structure of these fees to manage costs effectively.

The primary types of fees include:

Interchange Fees: Paid by the acquiring bank to the issuing bank for each card transaction. These vary based on card type, transaction method (card-present or card-not-present), and business type due to differing fraud risks.

Scheme Fees: Flat fees paid to card schemes like Visa or Mastercard to maintain network infrastructure and support card acceptance rules.

Processing Fees: Charged by PSPs like Adyen or Stripe for services such as transaction authorization, risk management, and customer support.

Acquiring or Commission Fees: Include markup (PSP's service fee) or blended rates (fixed fees covering specific payment methods).

Non-Transactional Fees: Calculated monthly on aggregated transactions, such as non-transactional scheme fees, with no markup from the PSP.

Other Fees: Include 3DS authentication fees, chargeback services, risk management services, and terminal-related fees (e.g., replacement or SIM card subscriptions).

Understanding these fees is crucial to budget accurately, forecast expenses, and negotiate better terms with PSPs. The complexity of payment processing, which appears seamless to customers, involves sophisticated backend operations that CFOs must master to optimize financial performance. If you want to learn more about the topic, check out our previous blog post on understanding payment fees.

How are costs in payments being billed?

Payment processing costs are billed through a combination of methods, with some deducted directly from transaction settlements and others invoiced separately. The attached payment lifecycle flowchart illustrates the flow of transactions and the associated fees.

What Transactions Incur Costs?

Costs are incurred at various stages of the payment lifecycle, as outlined in the flowchart:

Checkout: Processing fees are charged when a payment request is initially received.

Successful Authorization: Scheme fees apply for authorized transactions, including zero-auth and auth-adjustments.

Captured: Acquiring services fees (e.g., interchange, scheme, and markup) are applied when transactions are sent for settlement or settled.

Refund: Processing fees and refund fees are incurred for refund requests and completions.

Issuer/Wallet decline: Scheme fees and authorization fees are charged for non-settled transactions, such as those refused by the issuer, canceled by the merchant, or expired before capture.

Chargeback: Additional chargeback fees are incurred when a transaction is disputed and reversed.

These transaction stages trigger both predictable operational fees and occasional additional costs, depending on the outcome.

Expected vs. Unexpected Costs

Expected Costs:

Processing Fees: Consistently applied to received and refund transactions, forming a predictable portion of the billing cycle.

Payment Method Fees: Include interchange, scheme, and markup fees tied to settled transactions, calculated based on agreed rates and transaction volume.

Acquiring Services Fees: Deducted during settlement, these are expected based on the PSP's fee structure and card network policies.

These costs are typically outlined in the PSP contract and can be forecasted using historical transaction data.

Unexpected Costs:.

Non-Transactional Scheme Fees: Calculated monthly on aggregated volumes with a billing delay, making them less predictable without detailed reporting.

Chargeback and Refund Fees: Can occur unexpectedly due to customer disputes or refund requests, adding variability to the cost structure.

Rounding and Tiering Adjustments: Differences between deducted and calculated amounts due to rounding or tiered pricing can lead to surprises during reconciliation.

These costs require vigilant monitoring and reconciliation to manage effectively, as they may not align with initial settlement deductions.

How to reconcile PSP invoices?

Payment reconciliation is more than an operational necessity. For CFOs, it’s a vital process to ensure the accuracy of reported revenue, detect anomalies, and maintain trust in financial reporting.

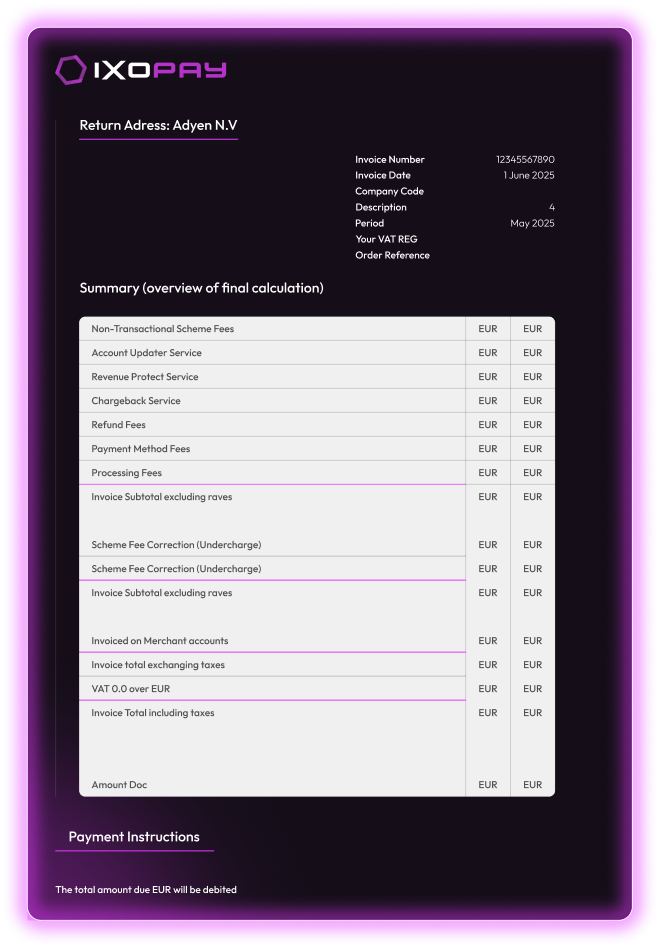

For example, this is the structure of a provider's invoice such as Adyen, which requires some deep understanding of fees and the composition of those for an exact fee allocation and reconciliation exercise.

Here's a step-by-step approach to reconciling payments effectively:

1. Gather All Payment Records

Start by collecting every relevant data source. This includes transaction data from your PSP, monthly invoices, settlement reports, internal sales systems, and your bank statements. Reconciliation only works when you're working from a complete picture.

2. Match External Transactions to Internal Records

Each payout from a payment provider should be mapped to the correct internal transaction. This involves linking the transaction ID, amount, currency, and payment method to your internal systems such as order management or accounting software.

3. Identify Discrepancies

Discrepancies can occur for several reasons. These may include timing delays, unprocessed refunds, chargebacks, incorrect fees, or batch settlements. Identifying them early reduces the risk of downstream reporting errors.

4. Investigate and Resolve Issues

Once discrepancies are flagged, investigate the root causes. Look into whether a refund was delayed, if a transaction was reversed without notice, or if a processing fee was misapplied. Work closely with your finance operations and support teams to resolve the issues and document any adjustments made.

5. Confirm Payout Totals

After transaction-level reconciliation, verify that the total payout amounts from each PSP align with what is shown in your bank statements. Any variances should be small, explained, and tracked.

6. Use Automation to Reduce Manual Work

Manual reconciliation across multiple PSPs can be time-consuming and error-prone. Automated payment reconciliation solutions can ingest data from different systems, apply matching logic, and highlight mismatches for review. This reduces the effort required and significantly speeds up monthly close cycles.

Best practices in understanding PSP fees

Payment service providers rarely offer a one-size-fits-all pricing model. Fees can vary depending on the region, payment method, transaction volume, and the provider's pricing structure. While some fees are transparent, others are buried in blended rates or hidden in monthly invoices. For finance leaders, staying on top of these costs is not just about minimizing spend – it's about ensuring accurate forecasting, identifying inefficiencies, and holding providers accountable.

Below are key practices to help you take control of your payment fee structure and maintain financial visibility.

1. Know the Fee Structure

PSPs typically charge a combination of fees. Understanding each type is foundational:

Merchant Discount Rate (MDR): The overall fee per transaction (usually a percentage of the transaction value).

Interchange Fees: Paid to the cardholder's bank.

Scheme Fees: Charged by card networks like Visa and Mastercard.

Acquirer Fees : The Acquirer's margin on top of other fees.

Other Fees: Can include setup fees, monthly maintenance, chargebacks, refunds, cross-border, and currency conversion fees.

Tip: Request a full fee schedule (or pricing sheet) from your PSP-including interchange and scheme fee distributions.

2. Understand Pricing Models

There are three common PSP pricing models:

Blended Pricing: A single fixed rate per transaction.

Interchange++ (IC++): Itemized pricing that separates interchange, scheme, and PSP markup; offers full transparency.

Flat Fees / Tiered Pricing: Often based on transaction type, volume, or risk.

Best Practice: If your volumes are high, IC++ is usually more cost-effective and transparent.

3. Analyze Regional Variations

Fees vary by geography and transaction type:

Domestic vs. Cross-border: Cross-border transactions incur higher interchange and scheme fees.

Card-present vs. Card-not-present: Online (CNP) transactions typically carry higher fraud risk and thus higher fees.

Card Type: Debit, credit, commercial cards, and premium cards often carry different interchange rates.

Tip: Segment transactions by type and region to uncover hidden cost drivers.

4. Benchmark Regularly

Compare your rates with industry averages or competitors.

Use available databases (e.g., Visa/Mastercard interchange tables) and PSP reports.

Best Practice: If you’re overpaying, use the benchmark data to renegotiate.

5. Evaluate All-in Cost of Ownership

Consider PSP fees in the context of other operational factors:

Integration and maintenance costs

Payment acceptance rate

Fraud management capabilities

Customer support and reporting tools

A PSP with slightly higher fees might be more valuable if it increases authorization rates or reduces fraud.

6. Negotiate Proactively

As your volume grows, renegotiation is key:

Ask for volume discounts.

Request IC++ if you’re currently on blended pricing.

Review and negotiate long-tail fees (e.g., chargebacks, refunds) and ask for caps.

Pro Tip: Bundle multiple services (e.g., fraud tools, multi-currency support) for better pricing leverage.

7. Use Transparent Reporting Tools

Choose PSPs that offer:

Detailed transaction-level reporting

Fee breakdowns per transaction

APIs for fee extraction and reconciliation

Best Practice: Use analytics to monitor your Effective Blended Rate over time and flag anomalies.

8. Integrate Fee Data with Your Analytics Stack

For deeper cost insights:

Match fee data with transaction and customer data

Monitor cost per customer, region, or product

Set up dashboards for real-time fee monitoring

Best Practice: Use out-of-the box payments observability and intelligence solutions such as IXOPAY.

9. Monitor Chargebacks & Penalties

Understand your chargeback fee structure and dispute process:

High chargeback ratios (>1%) can lead to penalties, increased fees, or account holds.

Tip: Invest in chargeback prevention tools and strong dispute resolution workflows.

10. Regularly Review & Optimize

Fees change over time due to:

Scheme updates (e.g., Visa/Mastercard fee changes)

Regulatory shifts (e.g., PSD2, IFR caps in Europe)

New card products or payment methods

Set a quarterly review process to audit PSP fees, especially if you operate across regions or use multiple PSPs.

How we display invoice data in IXOPAY

With IXOPAY you can see the invoice data or files that your payment service provider shares with you in a normalized format.

For example, we normalize the invoice structure for providers such as Adyen, by distributing the data items into specific dedicated table fields, so you can analyze the invoices data both on company or merchant account level, month over month with the fields in an original format.

You can build your own custom boards utilizing our Data Explorer and than you can share those custom boards with the rest of your team members. This can be especially helpful to receive a quick overview of your invoice items, within a few seconds instead of going back to a bunch of PDF files.

Make Payment Costs a Strategic Advantage

PSP fees may seem like a small operational detail, but for finance teams managing high volumes and multiple markets, they can have a meaningful impact on margins, forecasting accuracy, and financial transparency.

By breaking down how fees work, how they're billed, and how to interpret PSP invoices, CFOs and finance leaders can turn complexity into clarity. This understanding isn't just about compliance – it's about identifying hidden cost drivers, negotiating smarter, and uncovering opportunities to improve payment performance.

IXOPAY empowers you to do exactly that. From normalizing invoice data across providers to giving your team the tools to analyze, share, and act on cost insights, we help you stay in control of your payment data, without drowning in PDFs.

Book a demo to see how IXOPAY can simplify your fee management and unlock better financial decisions.